The bonded warehouse vs FTWZ question is one of the first big decisions every importer faces when goods land in India: where will this cargo sit, and when exactly do I have to pay duty on it? For most businesses, handing over the full customs duty the moment a container lands is a heavy, and often unnecessary, drain on working capital. That is especially true when the goods may be re-exported, sold gradually over several months, or are still waiting for a confirmed buyer. Paying everything upfront ties up cash you could be using elsewhere, which is exactly why getting the bonded warehouse vs FTWZ choice right matters so much.

This is exactly the problem that two very different facilities are built to solve: the customs bonded warehouse and the Free Trade Warehousing Zone, or FTWZ. On the surface they look almost identical, because both let you store imported goods without paying customs duty at the time of arrival. But that surface similarity hides a deep divide. The two are built on completely different laws, serve different kinds of trade, and carry very different cost structures the longer your goods stay in storage. Choose the wrong one and you can end up paying interest you never needed to, or locking export-bound cargo into a setup designed for domestic sales.

This guide explains what a bonded warehouse and an FTWZ actually are, how each one treats duty and storage time, where their real costs diverge, and, most importantly, a clear framework for settling the bonded warehouse vs FTWZ decision for your imports. By the end you will know which structure protects your working capital and matches the way your goods actually move.

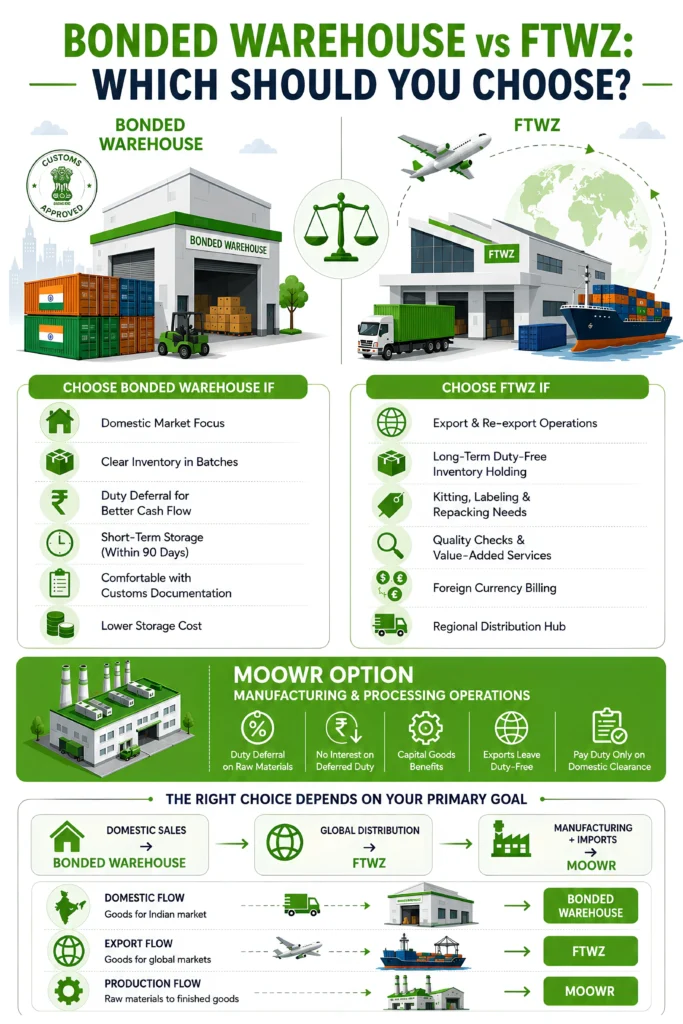

Quick verdict: The bonded warehouse vs FTWZ choice usually comes down to direction. If you import mainly for the Indian domestic market and want to defer duty until you sell, a bonded warehouse usually fits. If you are export-focused, run a regional distribution hub, or want to hold stock duty-free for a long time with value-added services, an FTWZ is generally the stronger choice.

What Is a Customs Bonded Warehouse?

A customs bonded warehouse is a secured facility, licensed and supervised by the customs authorities, where imported goods can be stored without the importer paying customs duty at the time the goods arrive. The key word is deferred, not waived. The duty liability does not disappear; it is simply postponed. It becomes payable only when the goods are finally cleared out of the warehouse for use in the domestic market, a step known as ex-bond clearance. Until that moment, the cargo sits “in bond,” legally under the control of customs even though it is physically held in a private or public storage facility.

The framework comes from the Customs Act, 1962, principally Sections 57 to 73. When goods are warehoused, the importer files an into-bond bill of entry and executes a bond, typically a triple-duty bond under Section 59, committing to pay the duty and to comply with the conditions of warehousing. That bond is the legal backbone of the entire arrangement. It is what allows customs to release physical possession of the goods while still holding a financial claim over them.

How a bonded warehouse works in practice

In day-to-day terms, the flow is straightforward. Your goods arrive at the port, and instead of clearing them for home consumption and paying duty there and then, you file to move them into a bonded warehouse. The goods travel to the facility under customs control. They sit there, duty unpaid, for as long as you need within the permitted period. When you are ready to sell into the Indian market (perhaps in batches as demand comes in), you file an ex-bond bill of entry for the quantity you want to release, pay duty on just that portion, and take it out. Anything still in the warehouse remains duty-deferred. This batch-by-batch clearance is one of the biggest practical advantages, because you pay duty in step with your actual sales rather than all at once.

Storage period and the 90-day interest clock

India generally allows goods to be warehoused for up to one year, with capital goods receiving more generous treatment and extensions possible in certain cases. But there is an important catch that many importers overlook when they first compare options. Under Section 61 of the Customs Act, interest starts to accrue on the deferred duty once goods have been stored beyond 90 days. So while a bonded warehouse defers your duty, it does not defer it for free indefinitely. Past the three-month mark, the clock starts ticking and an interest cost builds on top of the duty you will eventually pay. For fast-moving stock this rarely matters; for slow-moving or seasonal inventory, it can quietly erode the working-capital benefit you were chasing.

Types of bonded warehouses

The Customs Act recognises a few distinct categories. A public bonded warehouse, licensed under Section 57, is operated to store goods for multiple importers. A private bonded warehouse, licensed under Section 58, is appointed for a specific licensee to store its own imported goods. There are also special warehouses under Section 58A for certain sensitive categories of goods that require storage under the physical lock of customs. For most commercial importers working with a third-party logistics partner, the practical choice is between using space in a licensed public bonded warehouse or operating under a private licence.

Manufacturing inside a bonded warehouse: the MOOWR route

Ordinary bonded warehousing permits storage and only light operations such as sorting, repacking, labelling and similar activities that do not amount to manufacture. If you actually want to manufacture or carry out substantial operations on imported inputs while keeping the duty deferred, that is governed separately by Section 65 of the Customs Act, operationalised through the Manufacturing and Other Operations in Warehouse Regulations, 2019, commonly called the MOOWR scheme. Under MOOWR, a private bonded facility can import both raw materials and capital goods with customs duty fully deferred and, importantly, with no interest liability. Duty is paid only when finished goods are cleared into the domestic market, and goods that are exported leave duty-free. For manufacturers, MOOWR has become a powerful alternative to older export-promotion schemes, which is why it frequently comes up in any serious bonded-warehouse discussion.

What Is an FTWZ (Free Trade Warehousing Zone)?

A Free Trade Warehousing Zone is a different animal altogether. Where a bonded warehouse is essentially a storage mechanism layered over the Customs Act, an FTWZ is a complete trade ecosystem. It is a special category of Special Economic Zone (SEZ) created specifically for warehousing, trading and logistics activities, and it is governed by the SEZ Act, 2005, together with the SEZ Rules, rather than by the warehousing provisions of the Customs Act. If you want the policy background, our explainer on the genesis and objectives of FTWZs in India covers how the model came about.

The single most important thing to understand about an FTWZ is its legal status: for customs and tax purposes, an FTWZ is treated as deemed foreign territory. Goods inside the zone are regarded as if they have not yet entered India at all. That one legal fiction changes everything about how duty, time and tax behave inside the zone. You are not deferring an Indian duty liability that is already attached to the goods; the goods simply have not crossed the customs frontier into India yet. The duty event only triggers if and when the goods leave the zone and enter the Domestic Tariff Area (DTA), which is the rest of India outside SEZs and FTWZs.

How an FTWZ treats duty, tax and time

Because the goods are treated as outside India, there is no customs duty payable while they remain in the zone, and, unlike a bonded warehouse, there is no 90-day interest clock and no equivalent time pressure. Goods can be held duty-free for as long as your business needs, until you decide to move them into the domestic market. At that point, customs duty becomes payable, just as it would on any import. Activities and transactions conducted inside the zone also enjoy exemptions from local taxes, and one of the practical attractions for international businesses is the ability to bill and transact in foreign currency from within the zone. This makes an FTWZ particularly attractive as a regional hub, where a foreign supplier can hold stock close to Indian and South Asian customers without yet importing it.

What you can actually do inside an FTWZ

FTWZs are designed for far more than passive storage. Permitted activities typically include storage and warehousing, labelling, barcoding and re-labelling, kitting and bundling, repacking and re-palletisation, light assembly, quality inspection, and the consolidation or deconsolidation of shipments. Crucially, goods can be re-exported directly from the zone without ever attracting Indian customs duty, which makes the FTWZ a natural fit for businesses that import, add value, and send goods back out to other markets. This combination of duty-free holding and value-added services under one roof is what people mean when they call an FTWZ a one-stop trade ecosystem rather than just a shed with a customs seal.

The three-party model

Operationally, an FTWZ usually involves three parties: the zone unit operator who holds the FTWZ licence and runs the facility, the supplier or importer who places goods into the zone, and the customer who eventually takes them. Because the operator handles customs documentation, compliance and the value-added services inside the zone, importers, especially overseas ones without an Indian establishment, can use an FTWZ as a ready-made landing pad in India without building their own bonded infrastructure. The operator’s licence and systems do the heavy lifting.

Bonded Warehouse vs FTWZ: The Key Differences

Both facilities defer the moment you pay duty, and both can be operated by a third-party logistics partner. But the differences underneath, such as the governing law, the treatment of time, the interest exposure, and the kinds of activity allowed, are what should actually drive your decision. The table below lays the two side by side.

| Parameter | Customs Bonded Warehouse | FTWZ (Free Trade Warehousing Zone) |

|---|---|---|

| What it is | A licensed storage facility where imported goods sit duty-deferred until cleared. | An SEZ-class trade zone for storage, value-addition and re-export of goods, duty-free. |

| Governing law | Customs Act, 1962 (Sections 57 to 73); MOOWR, 2019 for manufacturing. | SEZ Act, 2005 and SEZ Rules; treated as deemed foreign territory. |

| Customs duty | Deferred; payable on clearance to the domestic market. | Not yet applicable; payable only on clearance from the zone to the DTA. |

| Interest on duty | Interest accrues after 90 days of storage (Section 61). | No interest; no time limit on duty-free storage. |

| Storage period | Up to about 1 year for most goods; longer for capital goods; extendable. | No fixed time limit until goods move to the DTA. |

| Taxes | GST/IGST applies on domestic clearance. | Exemptions on zone activities; foreign-currency billing allowed. |

| Permitted activities | Storage, sorting, repacking; manufacturing only under MOOWR (Sec. 65). | Storage, labelling, kitting, repacking, assembly, QC, consolidation, re-export. |

| Best suited to | Importers selling into the Indian market who want to defer duty until sale. | Export and re-export, regional hubs, long-term duty-free holding and value-addition. |

Read this bonded warehouse vs FTWZ table from the bottom up and a pattern emerges. A bonded warehouse is fundamentally domestic-facing: it is a way to bring goods into India but delay the duty bill until you sell them. An FTWZ is fundamentally trade-and-export-facing: it is a way to hold goods at the edge of India, add value, and decide later whether they go in or go back out, with no time pressure either way.

Bonded Warehouse vs FTWZ: Cost and Duty Implications

On a quick read, both options sound like “store now, pay duty later.” In a bonded warehouse vs FTWZ comparison, the difference becomes real when you factor in time and the cost of money. This is where many importers make an expensive assumption.

With a bonded warehouse, the 90-day interest rule under Section 61 is the variable to watch. For the first three months, deferral is clean. After that, interest begins building on the deferred duty for as long as the goods remain in bond. Picture a consignment carrying a sizeable duty liability that ends up sitting for seven or eight months while you work through slow domestic demand. The duty was deferred, yes, but you will pay it eventually plus several months of accrued interest. When importers compare a bonded warehouse to an FTWZ purely on storage rates, this interest line is the cost they most often forget, and it is precisely the cost an FTWZ does not impose, because inside the zone there is no Indian duty liability ticking in the first place.

An FTWZ has its own cost structure, of course. You pay the zone operator for handling, storage and any value-added services, and these zone charges can be priced at a premium to a plain warehouse because you are buying a compliance-managed, duty-free, export-ready environment, not just floor space. The trade-off is straightforward: an FTWZ removes duty-interest exposure and gives you indefinite duty-free holding, but you pay for the privilege through the operator’s service rates. For goods that move quickly into the domestic market, that premium may not be worth it. For goods that sit a long time, get re-exported, or need value-addition, the FTWZ economics usually win comfortably.

The deciding financial question is therefore not “which storage is cheaper per pallet,” but “how long will my goods sit, and where are they ultimately going?” The longer the dwell time and the more likely re-export becomes, the more an FTWZ’s no-interest, no-time-limit, duty-free model pulls ahead. The faster the domestic turnover, the more a bonded warehouse’s lower base cost and batch-clearance flexibility makes sense.

Bonded Warehouse vs FTWZ: Which Should You Choose?

In the bonded warehouse vs FTWZ debate there is no universally “better” option, only the option that fits how your goods actually move. Use the following as a practical decision guide.

Choose a customs bonded warehouse if…

- Your goods are primarily destined for the Indian domestic market, not re-export.

- You want to defer duty and clear stock in batches as you sell, conserving working capital.

- Your typical dwell time is short, comfortably within the 90-day window before interest applies.

- You want a lower base storage cost and are comfortable managing the bond and customs paperwork.

Choose an FTWZ if…

- Your business is export- or re-export-focused, or you serve regional markets from an India hub.

- You need to hold stock duty-free for a long, uncertain period without an interest penalty.

- You want value-added services such as kitting, labelling, repacking, assembly and QC, done on duty-free goods.

- You are an overseas supplier who wants an India landing pad without building your own bonded setup, ideally with foreign-currency billing.

Consider MOOWR if…

- You manufacture or carry out substantial operations on imported inputs and want duty deferral with no interest on both raw materials and capital goods, paying duty only on what is cleared domestically while exports go out duty-free.

Many businesses do not have to pick just one. A growing importer might run domestic stock through a bonded warehouse, hold export and regional inventory in an FTWZ, and put a manufacturing line under MOOWR, matching each goods flow to the structure that protects its margin best. The right answer is the one that mirrors the direction your goods travel and how long they wait before they get there.

How Genex Logistics Helps You Get It Right

The bonded warehouse vs FTWZ decision is rarely a one-line answer; it depends on your duty exposure, your dwell times, your export ratio and your value-addition needs. As a PAN-India third-party logistics and contract-logistics provider, Genex Logistics helps importers map their goods flows to the right structure and then runs the operation end to end, from customs clearance and freight forwarding to bonded storage, FTWZ-based handling and value-added services such as kitting, labelling and repacking.

Rather than forcing your goods into whichever facility is on hand, the goal is to match each flow (domestic, export and manufacturing) to the structure that best protects your working capital and speed. Talk to Genex about the right import-storage setup for your goods, and turn duty deferral into a genuine working-capital advantage.

Frequently Asked Questions

A bonded warehouse is a storage facility under the Customs Act where imported goods sit with duty deferred until they are cleared into the domestic market. An FTWZ is an SEZ-class zone, treated as deemed foreign territory, where goods are considered not yet imported into India, so duty applies only if and when they leave the zone for the domestic market, with no interest and no time limit while they remain inside.

Neither is universally better. An FTWZ is generally stronger for export-focused or re-export trade, long-term duty-free holding and value-added services. A bonded warehouse is often more cost-effective for goods bound for the Indian domestic market that turn over quickly, where you simply want to defer duty until sale.

Not while the goods remain in the zone. Because the FTWZ is treated as outside India for customs purposes, customs duty becomes payable only when goods are cleared from the zone into the Domestic Tariff Area. Goods re-exported directly from the zone do not attract Indian customs duty at all.

Most goods can be warehoused for up to about one year, with longer treatment for capital goods and the possibility of extensions. However, under Section 61 of the Customs Act, interest begins to accrue on the deferred duty once goods have been stored beyond 90 days.

Ordinary bonded warehousing allows only storage and light operations like sorting, repacking and labelling. Full manufacturing is possible under Section 65 of the Customs Act through the MOOWR scheme, which lets a private bonded facility import inputs and capital goods with duty deferred and no interest, paying duty only on goods cleared domestically.

An FTWZ is a specialised type of SEZ focused specifically on warehousing, trading and logistics rather than on manufacturing or services more broadly. It shares the SEZ legal framework and deemed-foreign-territory status, but is purpose-built for storing, handling and re-exporting goods.

Activities and transactions conducted within an FTWZ generally enjoy exemptions from local taxes, and foreign-currency billing is permitted. GST and customs duty become relevant when goods are cleared from the zone into the Domestic Tariff Area, where normal import taxation applies.

The Bottom Line

Bonded warehouses and FTWZs both answer the same instinct, which is not paying duty before you have to, but they answer it in fundamentally different ways. A bonded warehouse defers an Indian duty liability that is already attached to your goods, and rewards quick domestic turnover within the 90-day interest window. An FTWZ keeps your goods at the legal edge of the country, free of duty and time pressure, ready to be re-exported or value-added or eventually imported when it suits you. Match the structure to the way your goods actually move, whether domestic and fast or export-bound and patient, and the deferral stops being a paperwork technicality and becomes real money back in your working capital.

Note: Duty, interest and storage-period rules referenced here are based on the Customs Act, 1962 and related regulations. Confirm current rates and conditions with your customs house agent or advisor before acting.

Kapil Pathak is a Senior Digital Marketing Executive with over four years of experience specializing in the logistics and supply chain industry. His expertise spans digital strategy, search engine optimization (SEO), search engine marketing (SEM), and multi-channel campaign management. He has a proven track record of developing initiatives that increase brand visibility, generate qualified leads, and drive growth for D2C & B2B technology companies.